The Hare and the Tortoise: The race is not to speedy (XV). Diversification for growth not be dismissed.

… “The tortoise meanwhile kept going slowly but steadily”…

The hare and the tortoise, a fable by Aesop

In our last post, we began to explore the main notions of what it is corporate strategy, in terms of formulation. To formulate is nothing else than to state or condense in systematic terms or concepts, or explained in one word: “a framework”. So we are in the stage of formulating the current theory, explained in simple terms.

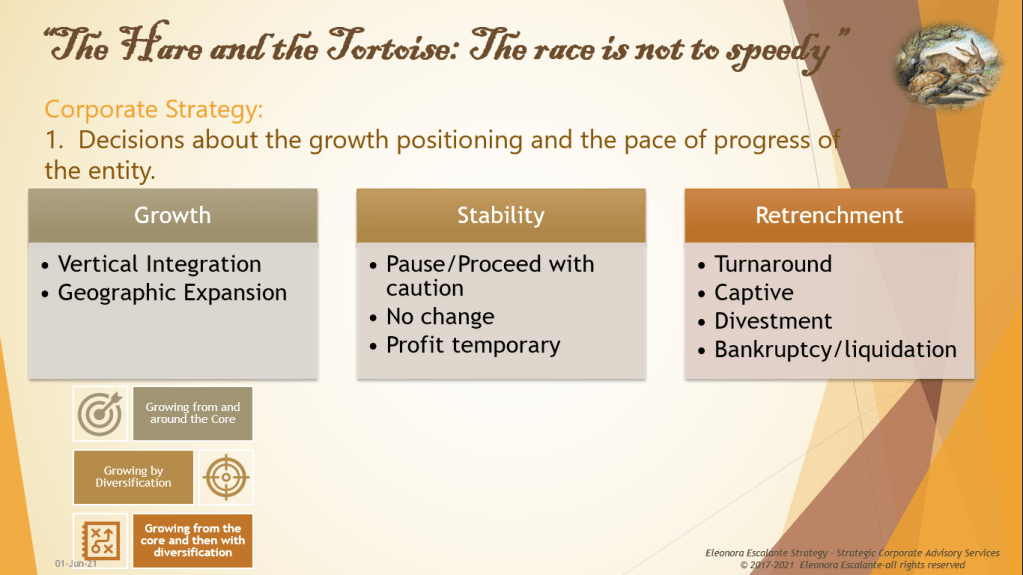

Racing for growth. In our last publication, we also introduced the three main general decision-making paths in corporate strategy:

- Decisions about the growth positioning and the pace of progress of the entity.

- Decisions about portfolio analysis.

- Decisions about corporate parenting.

We recently started with the first level of decision-making, and this level includes three paths to explore:

Growing, Stability, and Retrenchment. Some corporate strategy authors have coined different terms when it comes to teaching corporate strategy. Probably you will read the term corporate directional strategies, or a corporation directional strategy or you will see vertical integration/geographic expansion per separate subjects, as building blocks. But for us, since the corporate strategy is about decision-making at the top, we have to be congruent, and we baptized the corporate strategy formulation as a decision-making formulation. And, corporate strategy pre-establishes a previous roadmap design, measured in terms of time. That is why we will stick to the term “path” or “route”. You will comprehend why we have named, what other authors call “strategies”, to “paths”. In a couple of weeks, you will find out, when we end landing into the strategic reflection critique of the current theory. Be patient, we will arrive there, and we will also use examples, as you are used to reading from us.

For the time being, according to our buzzword, we are at the corporate strategy growth path decision-making level.

Let´s continue. Today is about subject number 2. Growing by diversification.

NUMBER TWO. Growing by diversification

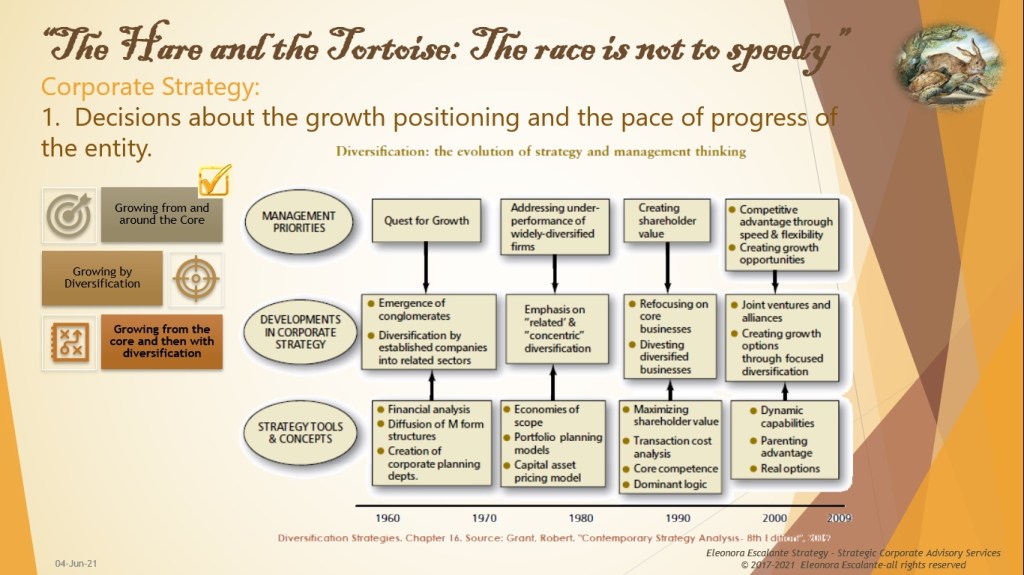

As you already know, we always start with at least a hint of the history from the past when it comes to diversification.

From the figure above, we can infer that diversification as a decision to grow, left the theater of management thinking a long time ago. The Golden age of Diversification happened after the end of WWII, between the years 1950 to 1980. And it was a major driver when it came to define the meaning of a corporation. It was during this time, in which the expansion of companies by using diversification, was a common recipe of success of corporate growth in all the advanced industrial nations.

According to Professor Robert Grant, “The 1970s saw the peak of the diversification boom, with the emergence of MNCs which were highly diversified”, As you can see in the figure, the trends in corporate strategy were changing, and by the 1990s and the 2000s, diversification fade away from the corporate thinkers, simply because value-based “maximizing shareholder value” took over the world of business, and “the core business” took over management, and divestments was the recipe applied.

What is diversification growth? Diversification comes from the verb diversify. To diversify means to give variety to your businesses. To extend business activities into disparate or dissimilar fields or industries, in which the two companies have different industries value chains.

Diversification at the corporate strategy level, could be related or unrelated between two companies of two different industries. Relatedness in diversification refers to the potential for sharing and transferring resources and capabilities between businesses. The degree of relatedness (related or unrelated) are the two extreme possibilities here, which are very interesting to comprehend. How can we measure the degree of relatedness between entities of two different industries when we decide to diversify? How to search the common thread (the essence of linkages) that connects two companies from two different industries? Is relatedness measured in terms of similarities between technologies and markets only? Or do they share similar operational value chains, even though are from different industries? Are the sources of value creation within a diversified firm coming from the ability to apply common general management capabilities, strategic management systems and resource allocation processes to the different businesses? How to recognize those synergies?

What to do to grow through diversification? Diversification is another way in which our entities can grow. Diversification almost disappeared from the texts of corporate strategy since the 2000 decade. But with the COVID19, I am sure diversification will be trendy again in management. In such an uncertain scenario as a health catastrophe, with globalization in place, to grow from the core is not feasible, unless your company belongs only to the essential local industries. When mobility is restrained, the rest of industries have been impacted tremendously. This is why I have to dedicate this post to all of those corporate strategists who almost killed diversification as a path for corporate strategy. Things will change after this pandemic.

Why to grow using diversification? During the age of diversification, the whole idea of growing through diversification was founded in the following reasons:

- Markets Saturation/Maturity: For stagnant or declining industries, and once there is no possibilities to grow by any other means, not even by inventing new technologies, because customers have pre-determined to don’t upgrade them anymore. Example: When the mobile industry participants will reach all the demand of 195 countries, and telecom companies’ network ultrawideband technology network infrastructure starts to be regulated worldwide to reduce the pace of the shift between each new internet network release (i.e. governments will not approve the 6G until 20 years later from now); then the telecom moguls industries will be on decline. If one of these entities decides to invest in the industry of agriculture, or in oil and gas, that is an unrelated diversification. If another telecom company decides to invest in social media platforms, then we are facing a related diversification.

- Risk Reduction. The desire to spread risks, or to don’t put all the eggs in the same baskets comes from here. With the pandemic, all the businesses from industries that required mobility or social interaction will start to think how to diversify their exposure to future pandemic force majeures.

- Creating value for Shareholders. In the 80s, the poor performance of the very diversified firms led to skepticism about the ability of the corporate strategists to manage and add value to its multiple diverse businesses. In addition, the theory of management of that time started to implement the term “cost efficiency”, for which there was a new emphasis on cost-cutting at the corporate level. As a result, at that time a wave of takeovers forced senior management to focus attention on Value-based strategies. In the 90s, the pressure of raiders and leveraged buyout firms triggered that the corporate head offices rifled for a Value-based approach in which the free cash flow was the correct measure of shareholder value, and those cash flows were discounted at each business-specific weighted cost of capital. The notion of core business came into the scene. The 90s shuddered the diversified corporations with a trend of breakups, restructurings, demergers, and refocusing takeovers. Porter´s essential tests to “create shareholder value” through diversification emerged, and for many, the diversification was considered as a sin. The three Porter “essential tests” to be applied in deciding to diversify to create shareholder value are:

- The Attractiveness test. The industries chosen for diversification must be structurally attractive or capable of being made good/nice looking and gorgeous.

- The Cost-of-entry test. The cost of entry must not capitalize all the future profits

- The Better-off test. The new unit must gain a competitive advantage from its link with the corporation or vice versa.

How to grow through diversification? The emphasis in diversification (regardless if the business is related or unrelated) is based on sound investment and value-oriented management in resource allocation, strategy formulation, and performance-management control. Once a company decides to diversify, this is usually because it is capable of having a true and committed Board of Directors, including a corporate directors` team which have built the aptitude and the skills required to manage it. To diversify, any company can do it with the same approaches described when growing from the core. I will only list them because we already defined them: green-field development, strategic alliances, exporting, licensing, franchising, joint ventures, mergers and acquisitions, production sharing, human capital management contracts, and turnkey projects. In addition, the diversification may expand in scope from domestic, multidomestic, regional, international, transnational, and global.

What are the benefits of diversification? Regardless if you choose to grow by a related diversification or an unrelated diversification (which is called a conglomerate), to answer the question of how to grow by diversification relies upon around three factors:

- Economies of scope: The benefits of diversification focus on how to profit from economies of scope in common resources, or reach cost economies from increasing the output of multiple products. For example, if a certain raw material is used in the production of two different products, and this input is available only in units of a certain size, then, a single firm producing both different products, can be able to spread the cost of the raw material for a large volume of output, and reduce the unit costs of both products. Economies of scope can be examined concerning three resources categories: Tangible resources used in joint production, as raw materials, distribution networks, research laboratories, information databases, call centers, provision of support services, etc.; Intangible resources as brands, corporate reputation, technologies, etc.; and Organizational Capabilities, such as business intelligence, market analysis, advertising, retail management or general management capabilities.

- Economies from Internalizing transactions: For diversification to yield competitive advantage requires the presence of transaction costs that discourage the firm from selling or renting the use of specific resources to other firms. Transaction costs include the costs involved in drafting negotiating, monitoring, and enforcing contracts for example. The costs of internalization consist of the management costs of establishing and coordinating the diversified business. Examples of high transaction costs abound in intangible resources such as brand names, technologies, development of software for specific tailor-made testing procedures, etc.

- Internal Capital Markets: This is the case, of diversified companies that decide to establish an internal bank (or financial services business) to use a common internal banking facility for all the diversified businesses. The benefit of a common treasury, develop structured finance, manage the leasing, trading capabilities and raise financial instruments in capital markets, allows not only cost savings but some degree of independence and quick response when financing is needed.

- Internal Labor Markets: Cost savings happen when a diversified company can do the internal transfer of employees between different businesses. The costs to hire a new employee are always high, so the possibility to use high caliber employees (specialists, managers) and transfer from elsewhere within the corporation to other divisions, is less costly than to hire a new candidate, which will require be trained for several years. The broader set of opportunities available in a diversified company (such as Nestle, Unilever, HP), as a result of an internal transfer, may also result in attracting higher caliber employees, which know in advance that an entry-level is accompanied by at least 2 years internal rotational training development.

- Information Advantages: The amount of information that a corporate head office of a diversified entity can hold is not only multiplied in terms of the manufacturing details coming from each business unit but also when it comes to reallocating financial capital and labor. The diversified firm that is engaged in permeating employees between different positions and different businesses, can build aggregated information flows between individuals, that may work together better as teams.

Number 3. Growing from the core and then with diversification.

To be continued. Have a happy weekend. Enjoy!

Bibliography utilized to get some ideas when writing today.

https://www.pearson.com/uk/educators/higher-education-educators/program/Wheelen-Strategic-Management-and-Business-Policy-Globalization-Innovation-and-Sustainability-Global-Edition-14th-Edition/PGM1079024.html

https://www.wiley.com/en-us/Contemporary+Strategy+Analysis%3A+Text+and+Cases+Edition%2C+9th+Edition-p-9781119120841

https://www.jstor.org/stable/4165132?seq=1

Disclaimer: Illustrations in Watercolor are painted by Eleonora Escalante. Other types of illustrations or videos (which are not mine) are used for educational purposes ONLY. Nevertheless, the majority of the pictures, images, or videos shown on this blog are not mine. I do not own any of the lovely photos or images posted unless otherwise stated.