Leg 3. From Cape Town to Melbourne (III). Without resources what can we do?…

Good afternoon. Today´s topic is Resources of the firm. I pray for the seven teams at the Volvo Ocean Race 2017-2018 could be safe and moving out from the strong Southern Ocean storm… I do hope they can be safe.

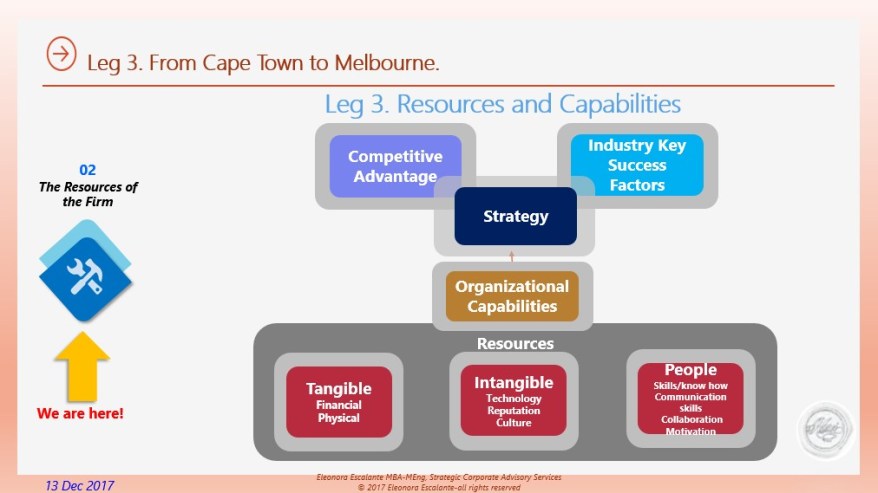

It is important to distinguish between the resources and the capabilities of the firm: Resources are the productive assets owned by the firm and its people. Resources are the basic units or items such as financial capital, equipment, the skills of individual employees, patents, branding, reputation, technology, etc. Capabilities are the protocols in which resources work together, or what the firm can do with its resources. Individual resources by themselves do not confer competitive advantage; they must work together to create organizational capability. It is a capability that is the essence of superior performance. Today we will dedicate some time to Resource Analysis.

Resources are the productive assets owned by the firm and its people. Resources are the basic units or items such as financial capital, equipment, the skills of individual employees, patents, branding, reputation, technology, etc. Capabilities are the protocols in which resources work together, or what the firm can do with its resources. Individual resources by themselves do not confer competitive advantage; they must work together to create organizational capability. It is a capability that is the essence of superior performance. Today we will dedicate some time to Resource Analysis.

The following figure shows the relationships among resources, capabilities, strategy and competitive advantage.

It is a mistake to believe that a resource analysis is easy. It is an error to think that by asking our clients for financial statements we will solve the resources analysis as if we are doing an annual inventory.  I always recommend analysts to be very delicate and refine their resources analytical processes. Resource Analysis is not making a list of financial items from financial statements. No such document exists within the accounting or management information systems of most corporations. The corporate balance sheet provides a limited view of a firm’s resources, and usually brings a partial and distorted snapshot of firm´s assets. Moreover, the balance sheet comprises mainly financial and physical resources. A useful starting point is to classify the resources in three groups: tangible, intangible, and people talents (I don´t like to use the term human resources, personally). Today we will cover the first two and for my next post, we will share the third one, people talents.

I always recommend analysts to be very delicate and refine their resources analytical processes. Resource Analysis is not making a list of financial items from financial statements. No such document exists within the accounting or management information systems of most corporations. The corporate balance sheet provides a limited view of a firm’s resources, and usually brings a partial and distorted snapshot of firm´s assets. Moreover, the balance sheet comprises mainly financial and physical resources. A useful starting point is to classify the resources in three groups: tangible, intangible, and people talents (I don´t like to use the term human resources, personally). Today we will cover the first two and for my next post, we will share the third one, people talents.

Tangible Resources

Tangible resources are the easiest to identify and evaluate: financial resources and physical assets are identified and valued in the firm’s financial statements.  Yet balance sheets are renowned for their propensity to obscure strategically relevant information and to distort asset values. Historic cost valuation can provide little indication of an asset’s market value. It is important to help our financial analysts with criteria guidelines about how to clean the financial statements properly. As Doctor Abraham Briloff from Baruch College said: “Financial statements are like fine perfumes to be sniffed but not swallowed”. I learned it is important to go to the cash flow statements and look at the footnotes for each accounting item first. It is easier when the financial statements are in IFRS versus local standards.

Yet balance sheets are renowned for their propensity to obscure strategically relevant information and to distort asset values. Historic cost valuation can provide little indication of an asset’s market value. It is important to help our financial analysts with criteria guidelines about how to clean the financial statements properly. As Doctor Abraham Briloff from Baruch College said: “Financial statements are like fine perfumes to be sniffed but not swallowed”. I learned it is important to go to the cash flow statements and look at the footnotes for each accounting item first. It is easier when the financial statements are in IFRS versus local standards.

However, the primary goal of resource analysis is not to value a company’s assets but to understand their potential for creating competitive advantage. For example, Facebook shows information about its property, plant, and equipment for a total amount of 8,591 million USD.

To know this amount of $8,591 million USD is of little use in assessing their strategic value.

My personal Facebook Timeline.

To assess Facebook’ ability to compete effectively in the Internet and Software services Industry, we need to know about the composition of these assets: the type of assets in which Facebook invests, the location of land and buildings, the types of network and equipment, what is the age and type of equipment, where and why are building new facilities, how flexible are they with regard to their new expansion plans by building these new assets, etc. Once we have fuller information on a company’s tangible resources we explore how we can create additional value for them.

Professor Robert Grant recommends to address two key questions:

- What opportunities exist for economizing on their use of finance, inventories, and fixed assets? It may be possible to use fewer resources to support the same level of business or to use the existing resources to support a larger volume of business.

In the case of Facebook Inc., and without knowing this company details, there may be opportunities for consolidating administrative offices and service facilities. Facebook Inc. has been in expansion mood. As Facebook grows, its data center requirements are growing along with it. Facebook’s existing U.S. data centers are in Oregon, North Carolina, and Iowa.

Centers in Fort Worth, Texas and Los Lunas, New Mexico are currently under construction, and Facebook announced plans for another site in Papillon, Nebraska in April this year. Recently in August, the company announced a new data center in New Albany, Ohio. As of the third quarter of 2017, Facebook had 2.07 billion monthly active users. We must ask ourselves how Facebook has pursued growth within the industries that support the company?. Are the company investments (recent CAPEX) enough to support the turnover? Why does the company invest in the USA and other international facilities?

- What are the possibilities for employing existing assets more profitably? Could Facebook generate better returns on some of its data centers? Should Facebook seek to redeploy its assets from one region to another one? How can Facebook re-target and re-enter the Chinese market after it was banned in July 2009? Is that possible? How would the company reduce costs? Are the recent acquisitions employed in a way that helps them to get a larger volume of subscribers?

Intangible Resources

For most companies, intangible resources are more valuable than tangible resources. Over time, working capital, fixed capital and other tangible assets are becoming less important to the firm both in value and as a basis for competitive advantage.

Yet, in company financial statements, intangible resources remain largely invisible— particularly in the U.S. where R&D is expensed. The majority of firms show balance sheet intangible items restricted to Goodwill arising from acquisitions and capitalized R&D Expenditures. Accounting book values usually bear little relationship to the true value of the firm´s resources. In many cases, the most important resources of the company may be invisible and nonobvious. The exclusion or undervaluation of intangible resources is a major reason for the large and growing divergence between companies’ balance-sheet valuations (“book values”) and their stock-market valuations. I have prepared a slide with the top 15 companies (with the largest market capitalization – with data from yesterday 12dec2017).

If you wish to see the last slides in PDF format, click here: Eliescalante Leg 3 Resources of the firm. part 1.

As you can read above, the top five largest companies in the world by market capitalization are Apple Inc., Alphabet Inc., Microsoft, Amazon, and Facebook. As you can see, the top 5 companies in the world are not banks neither traditional brick and mortar retailers. The price market per share to book value per share is different for each of them (all the data is from Fidelity.com). The price-to-book ratio (P/B Ratio) is a ratio used to compare a stock’s market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter’s book value per share. Why do we use the P/B ratio?. A company with a very high share price relative to its asset value is likely to be one that has been earning a very high return on its assets. Any additional good news may already be accounted for in the price. That is the case of Amazon and Alibaba, Microsoft, Facebook and Apple Inc.

Other intangible resources are brand names. ![]() Brand names and other trademarks are a form of reputational asset: their value is in the confidence they instill in customers. Different approaches can be used to estimate brand value (or “brand equity”). Two variables are critical to the valuation of reputation: (1) The size of the price premium that reputation will sustain the product and market scope of which reputation can be deployed. (2) The value of a company’s brand can be increased by extending the range of products over which a company markets its brands.

Brand names and other trademarks are a form of reputational asset: their value is in the confidence they instill in customers. Different approaches can be used to estimate brand value (or “brand equity”). Two variables are critical to the valuation of reputation: (1) The size of the price premium that reputation will sustain the product and market scope of which reputation can be deployed. (2) The value of a company’s brand can be increased by extending the range of products over which a company markets its brands.

Reputation may be attached to the company because of several reasons: for supplying quality products, for treating customers fairly, for being a reliable customer to its suppliers, for developing their employees, or even for being a socially responsible entity with the community. The reputation it is also attached to a company in the form of brand recognition and loyalty.

For example, in the future, Facebook can exploit some opportunities from applying their single brand to a wide range of products. The Like facebook Icon is extremely appealing, even several presidents and important personalities utilize them frequently (with exception of the countries where the Like thumbs-up is said to have various negative meanings such: West Africa, some countries in South America, Iran, Sardinia, Israel, Thailand, Afghanistan, Italy, and Greece).

Facebook can exploit some opportunities from applying their single brand to a wide range of products. The Like facebook Icon is extremely appealing, even several presidents and important personalities utilize them frequently (with exception of the countries where the Like thumbs-up is said to have various negative meanings such: West Africa, some countries in South America, Iran, Sardinia, Israel, Thailand, Afghanistan, Italy, and Greece).  But Facebook can use their LIKE Icon, to extend the Facebook brand to other diversified products not linked to technology, for example, apparel, caps, sports gears, coffee mugs, and other technology equipment. There are many examples, of companies that have succeeded in building strong consumer brands have had a powerful incentive to diversify—for example, Nike, Coca-Cola, Harley Davidson, Starbucks, etc.

But Facebook can use their LIKE Icon, to extend the Facebook brand to other diversified products not linked to technology, for example, apparel, caps, sports gears, coffee mugs, and other technology equipment. There are many examples, of companies that have succeeded in building strong consumer brands have had a powerful incentive to diversify—for example, Nike, Coca-Cola, Harley Davidson, Starbucks, etc.

Like reputation, technology has been always considered as an intangible asset whose value is not evident from most companies’ balance sheets. But I believe it has to be better classified and it should have a separate segment. With the emergence of digital technologies and the fact that many companies backbone is technology related, probably in the near future, this item has to be re-classified. A central issue in appraising technological resources is ownership.

Intellectual property—patents, copyrights, trade secrets, and trademarks—comprise technological and artistic resources where ownership is defined in law. Since the 1980s, companies have become more attentive to the value of their intellectual property.

This is all for today. On my next post, we will continue with People Talents as a key Resource for the firm. Thank you.

“Financial statements are like fine perfumes to be sniffed but not swallowed”. A. Briloff.

Source References:

http://www.wiley.com/WileyCDA/WileyTitle/productCd-1119120845.html

https://www.stock-analysis-on.net/NASDAQ/Company/Facebook-Inc/Analysis/Property-Plant-and-Equipment

http://money.cnn.com/2017/08/15/technology/facebook-ohio-data-center/index.html

https://www.statista.com/statistics/264810/number-of-monthly-active-facebook-users-worldwide/

http://www.datacenterknowledge.com/data-center-faqs/facebook-data-center-faq

https://www.investopedia.com/articles/fundamental/03/112603.asp

https://www.fidelity.com/?bar=p

https://www.pwc.com/gx/en/audit-services/assets/pdf/global-top-100-companies-2017-final.pdf

Disclaimer: All the pictures or videos shown on this blog are not mine. I do not own any of the lovely photos posted unless otherwise stated.