Entrepreneurs without Money XXXIII: El Salvador possible entrepreneurship journey with China. Financial Context (Part C).

Good afternoon. Wishing you a lovely Wednesday. Today is the turn of understanding why the cost of capital has to be determined when appraising the potential profitability of foreign investments. And the Cost of Capital definition and calculation is fundamental. On my last publication, we went through the three motivations or intentions of developed nations to give or invest in developing countries. Do you remember? 1) Altruism-humanitarian aid; 2) Win-Win; 3) Economic Expansion only. In the case of China, we have to understand the motivations of China to cooperate or to invest in El Salvador.

Good afternoon. Wishing you a lovely Wednesday. Today is the turn of understanding why the cost of capital has to be determined when appraising the potential profitability of foreign investments. And the Cost of Capital definition and calculation is fundamental. On my last publication, we went through the three motivations or intentions of developed nations to give or invest in developing countries. Do you remember? 1) Altruism-humanitarian aid; 2) Win-Win; 3) Economic Expansion only. In the case of China, we have to understand the motivations of China to cooperate or to invest in El Salvador.

If the motivations are pure altruism or humanitarian aid, the “cost of capital” is not the financial measure to utilize. There are other financial measures linked to social impact used by the United Nations organization systems or humanitarian aid agencies for this purpose.  For example, let´s suppose that the AECID (The Spain Aid Cooperation Agency) decides to provide non-reimbursable funds for the installation of potable water in 40 Salvadoran villages. The fact is that AECID is giving a “present”. And AECID provides these funds through the Central Government of El Salvador or directly to the 40 municipalities or boroughs. Since the project is “a grant”, the cost of capital is not the right measure to use, unless we wish to compare the same project from different donors. The transfer of funds from Spain to El Salvador is merely a gift. Each grant or non-reimbursable funds from Spain may or maybe not tied up to certain Spanish ESG (environmental-social-governance) impact conditions or standards. Usually, grants from foreign countries are entwined with technical assistance which includes training. Sometimes grants are tangled with the supply of raw materials or equipment or technology or certain quota of employees from the donor country.

For example, let´s suppose that the AECID (The Spain Aid Cooperation Agency) decides to provide non-reimbursable funds for the installation of potable water in 40 Salvadoran villages. The fact is that AECID is giving a “present”. And AECID provides these funds through the Central Government of El Salvador or directly to the 40 municipalities or boroughs. Since the project is “a grant”, the cost of capital is not the right measure to use, unless we wish to compare the same project from different donors. The transfer of funds from Spain to El Salvador is merely a gift. Each grant or non-reimbursable funds from Spain may or maybe not tied up to certain Spanish ESG (environmental-social-governance) impact conditions or standards. Usually, grants from foreign countries are entwined with technical assistance which includes training. Sometimes grants are tangled with the supply of raw materials or equipment or technology or certain quota of employees from the donor country.

German KfW has signed a loan agreement for 500 million euro, about Rs 3,750 crore, for the metro project, which is expected to be fully operational by March 2019. Source: https://www.business-standard.com

If the motivations to invest in developing economies is through win-win projects, the cost of capital has to be calculated. It is important when the funds provided represent a financial product such as a loan, guarantee or hedging financing. The win-win projects are usually given to the receiver public sector or private-public partnerships. And they may or may not include some part of grants-non reimbursable funds. These win-win projects are focused to improve one or various causes of national-global poverty localized systemically on the public sector or public institutions. For example, projects which tackle corruption, climate change mitigation, improving the productivity and competitiveness of certain ministries such as the Judicial-Law Enforcement, public sector utilities, highways-bridges, or even municipality infrastructure projects such as a new Metrorail, or an airport, etc.

Even though these projects are not “free lunch”, and all of them go to the public sector, there are some funds destinated to Private-Public Partnerships. The “win-win” projects are usually financed through development banks. Examples of these institutions are the KFW (German Development Bank), or the World Bank through its public sector division called International Bank for Reconstruction and Development (IBRD). The development banks offer an ample range of financial products such as equity, loans, guarantees (political or insurance).

Even though these projects are not “free lunch”, and all of them go to the public sector, there are some funds destinated to Private-Public Partnerships. The “win-win” projects are usually financed through development banks. Examples of these institutions are the KFW (German Development Bank), or the World Bank through its public sector division called International Bank for Reconstruction and Development (IBRD). The development banks offer an ample range of financial products such as equity, loans, guarantees (political or insurance).

If the motivations to invest in a developing economy are purely commercial or for economic expansion only, these last type of projects are called Foreign Direct Investments (FDIs). FDIs are usually initiatives of the private sector from a developed country or from a multinational corporation (MNC) which decides to invest in an emerging or developing economies. These companies look for sources of funds from commercial banks or development financing institutions. The risks to investing in developing countries are higher, and in consequence, the MNCs try to find financial resources at the private sector arms of development banks. I.e. the private sector financing division from the World Bank is the IFC (International Finance Corporation).

If the motivations to invest in a developing economy are purely commercial or for economic expansion only, these last type of projects are called Foreign Direct Investments (FDIs). FDIs are usually initiatives of the private sector from a developed country or from a multinational corporation (MNC) which decides to invest in an emerging or developing economies. These companies look for sources of funds from commercial banks or development financing institutions. The risks to investing in developing countries are higher, and in consequence, the MNCs try to find financial resources at the private sector arms of development banks. I.e. the private sector financing division from the World Bank is the IFC (International Finance Corporation).

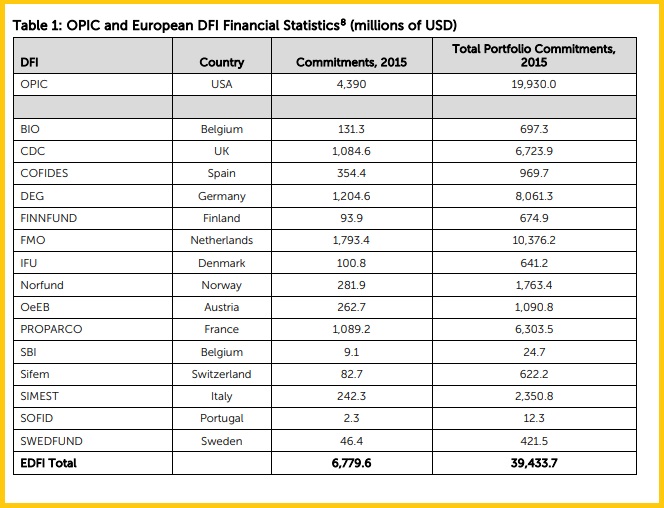

These development financial institutions offer an ample range of financial products such as equity, loans, guarantees (political or insurance). The DFIs are usually catalyzing co-investments and provide expertise. The Development Financial Institutions can be: 1) National or international development finance institutions (IFIs), and 2) Multilateral DFIs.

“The National or International DFIs are specialized development banks or subsidiaries set up to support private sector development in developing countries. They are usually majority-owned by national governments and source their capital from national or international development funds or benefit from government guarantees. This ensures their creditworthiness, which enables them to raise large amounts of money on international capital markets and provide financing on very competitive terms” (OECD). The China Development Bank is a national and international IFI (international finance institution).

Source: “Development Finance Institutions Come of Age: Policy Engagement, Impact, and New Directions”. Center for Strategic and International Studies (CSIS)

“Multilateral DFIs are private sector arms of international financial institutions (IFIs) that have been established by more than one country, and hence are subject to international law. Their shareholders are generally national governments but could also occasionally include other international or private institutions. These institutions finance projects in support of the private sector mainly through equity investments, long-term loans, and guarantees. They usually have a greater financing capacity than bilateral development banks and also act as a forum for close co-operation among governments” (OECD). The main multilateral DFIs include:

AFDB (African Development Bank)

ADB (Asian Development Bank)

EBRD (European Bank for Reconstruction and Development)

EIB (European Investment Bank)

IDB (Inter-American Development Bank)

IFC (International Finance Corporation) – I worked here!

ISDB (Islamic Development Bank)

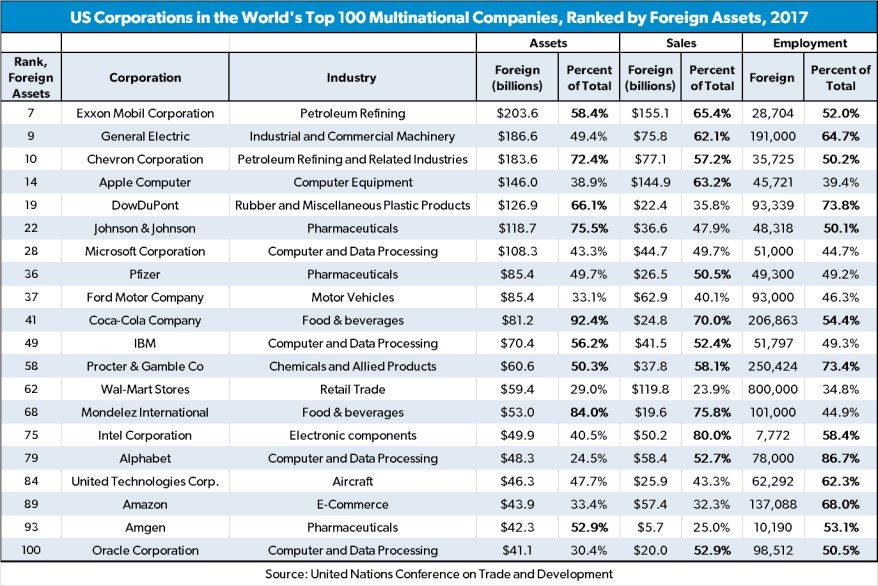

Now that we have understood who are the financing players, let´s explore some examples: If IKEA wishes to open new stores in Latin America, this Swedish conglomerate can use development financing sources of funds or commercial banks funds. It is up to each private company to decide. Other examples are TELMEX and AES expansion in Central America. I.e. AES borrowed money from a multilateral to buy the distribution electricity companies in El Salvador a couple of decades ago. Both companies have done investments in the region using financing from DFIs or commercial banks to buy existing local national telephone or electricity distribution companies when the local governments decided to privatize these utilities. The rationale behind development financial institutions (DFIs) is to create jobs, boost economic growth at the same time than raising the institutional standards of the developing nation by fighting poverty and climate change. When MNC´s wish to help to reduce the causes of poverty in developing nations, they must choose some part of their financing structure with a DFI. To my understanding, commercial banks don´t help to improve the institutional weaknesses of developing economies, meanwhile the DFI´s financing promise to help to change them.

Source: World Investment Report 2017, a report produced annually by the United Nations Conference on Trade and Development (UNCTAD)

Millicom (TIGO) is another example of FDI in emerging markets. The Luxembourg based group have expanded their mobile operations (in greenfield mode or by acquisitions) in several emerging countries, and they have used funds from development financing entities too.

Source: https://www.economist.com/briefing/2018/10/04/chinese-investment-and-influence-in-europe-is-growing

For all these MNCs investments, the financial measure of the cost of capital is extremely relevant. None of these corporations will invest their money unless those projects can yield economic rent or excess returns that lead to positive net present values. The focus for them is to perform a competitive analysis and apply financial value creation techniques to know if those returns are in excess of required by the shareholders. The cost of capital is, therefore “key”.

In the financial context, we seek to determine the cost-of-capital figures for several investments scenarios. What is the cost of capital? Is the required rate of return for a specific foreign project. It is the minimum risk-adjusted return required by shareholders of the firm for undertaking this investment. It is the basic measure of financial performance. Unless the investment generates sufficient funds to repay suppliers of capital (banks and equity investors) the firm´s value will suffer. This return requirement is met only if the net present value of future project cash flows, using the project´s cost of capital as the discount rate, is positive.

The CAPM or Capital Asset Pricing Model (CAPM) helps us to calculate the project-specific required return on equity based on modern capital market theory. We will dig in this theme on my next publication.

To be continued… Stay tuned. Thank you.

Source References utilized for this article:

http://www.cooperacionespanola.es/sites/default/files/03_sintetico_online_en.pdf

http://www.oecd.org/dac/stats/development-finance-institutions-private-sector-development.htm

https://read.oecd-ilibrary.org/development/development-co-operation-report-2014_dcr-2014-en#page60

https://csis-prod.s3.amazonaws.com/s3fs-public/publication/161021_Savoy_DFI_Web_Rev.pdf

https://unctad.org/en/Pages/DIAE/World%20Investment%20Report/World_Investment_Report.aspx

https://www.wiley.com/en-us/Multinational+Financial+Management%2C+10th+Edition-p-9781118572382

Disclaimer: All the presentation slides shown on this blog are prepared by Eleonora Escalante MBA-MEng. Nevertheless, all the pictures or videos shown on this blog are not mine. I do not own any of the lovely photos or images posted unless otherwise stated.