Leg Zero: Pressure from Substitutes: Porter´s Industry Analysis Model. Part V.

Today I will like to continue with the Threat of Substitutes Porter´s Force.

I set up the table with “Toys R Us” example because I wished to share with you a clear example of this second Porter´s force. In my own opinion “Toys R Us” current weak financial results started a long time ago. Even though they filed under Chapter 11 just a week ago, I doubt “Toys R Us” will disappear from the world map. It can´t happen overnight. The company still sells products but must walk through a painful restructuring phase. But if they wish to change its territory, to be successful in Europe, and continue operating there, they will have to modify their business model and value proposition accordingly to the new needs and wants of the kids of the future and their parents. Their value proposition will have to be adjusted as much as their client’s requirements of this new century. Simply we have to admit, times change.

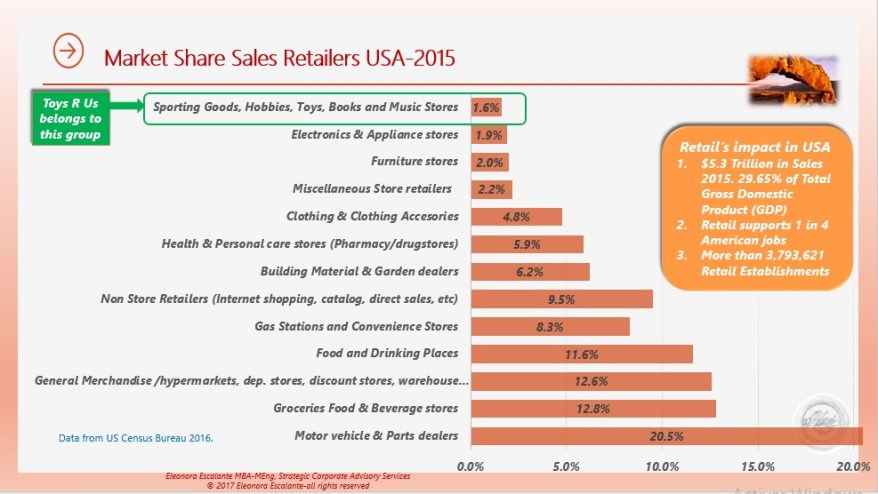

One of the reasons why “Toys R Us” did not reach financial positive results for a long time is related to its own position in the retailing industry. The retail industry is a sector of the economy that is comprised of individuals and companies engaged in the selling of finished products to end-user consumers. Multi-store retail chains, discount sales, motor -vehicle parts, healthcare products, gas stations and even restaurants are part of the retail trade. In the USA the retailers’ industry is as wide and big as the ocean. According to the US Census Bureau (Annual Retail Trade Survey), for the year 2015, it represented $5.35 Trillion USD in sales ($5,350,508 MUSD) or one-third of the USA 2015 GDP. The US Census Bureau has classified the retailers in 13 groups. The company “Toys R Us” is part of the retailers’ industry group called “Sporting goods, toys, hobby, book, and music stores” (which represents 1.6% of the total retailers’ sales per year), and specifically under the sub-industry group “Hobby, Toys and Games Stores”.

To see this slide in PDF, click Here: USA 2015 Retailer Industry Market Share: market share retailers

From there, we can observe that “Toys R Us” is positioned in the tiniest of the retailers’ industry groups.

Almost all the rest of the retailer industry groups can or are able to sell toys (with exception of motor vehicle-part dealers). Let´s think about which are “Toys R Us” substitutes: As a toy retailer, any of the other retailers is a substitute for this company!. We can buy toys anywhere. Hypermarkets sell toys. Discount department stores sell toys. Grocery Supermarkets sell toys. Even Gas Stations sell toys too!

Tonka Classic Steel Mighty Dump Truck FFP is sold at $22.99 in Amazon.com

“Toys R Us” started to lose its competitive advantage exactly since the founder Charles Lazarus stepped away from it in 1994. By the mid-1990s, “Toys R Us” started to lose sight of its own position in its own industry. Why? Because when Charles Lazarus was the leader of the company, he founded it as a Toys Discount Supermart. And its own industry is “Hobby, Toys and Games Stores”. But with the appearance and emergence of new incumbents, such as big discount retail chains as Walmart and Target or other general merchandise discount stores, “Toys R Us” instead of focusing to do a product differentiation strategy in their own industry apparently did the move to compete directly with other retailers´ substitutes. I have the hunch, “Toys R Us” was trapped to compete in so many different industries… “Toys R Us” was competing with each retailer substitute group they could. And, instead of focusing to compete with their own competitors of their own industry (Hobby, Toys and Games Stores), “Toys R Us” decided to compete with their substitutes, losing sight of its own scale and industry group. The threat of substitutes was so high, super higher. The 2015 annual sales of the “Hobby, Toys and Games Stores” sub-industry group represents 0.3% of the total retail trade $5,350,508 MUSD.

Dickie Toys Air Pump Dump Truck 11″ for $11.99 at Target.com

To see this slide in PDF, click here: retailer substitutes

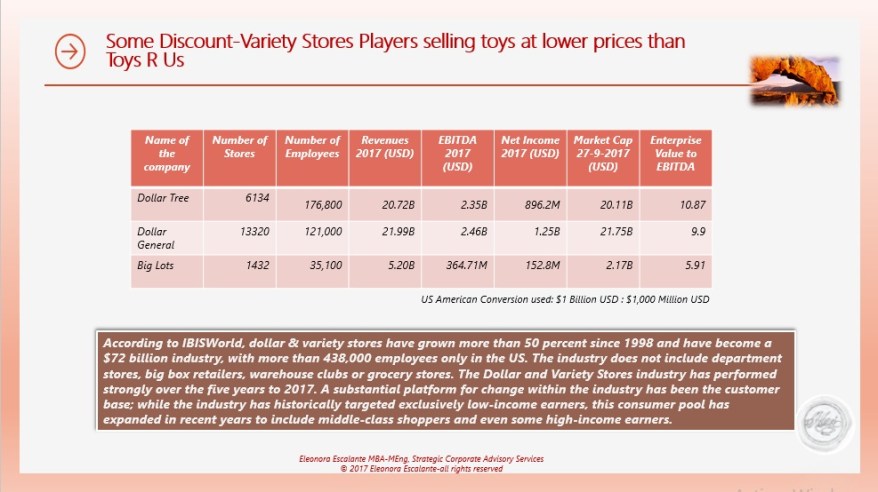

Let´s dig a little bit more about other “Toys R Us” retailer substitutes, as we published yesterday: what was happening with them during the last 30 years? The Discount & Variety stores grouped under Other General Merchandise Stores, the Warehouse Club stores, Supercenters and Non-Store Retailers have been growing during the last 25 years. Companies as Dollar Tree, Dollar General, and Big Lots have grown dramatically, particularly during the last decade. Discount Department stores as Walmart, Target, and Costco have also been growing steadily. All “Toys R Us” retailers´substitutes are also selling toys at lower prices. More than 90% of those toys are from China and sometimes, we can find them in a Dollar discount store for less than $2.00 dollars. During the last 25 years, toy retailers´ substitutes became direct competitors for “Toys R Us”. For “Toys R Us” it was impossible to compete with substitutes of lower cost. In this context, what happened to “Toys R Us” business model?

To see this slide in PDF, click here: discount stores substitutes

Yesterday I left several opened questions. Do you believe the reasons why “Toys R Us” filed for Chapter 11 Bankruptcy last week are: (1) its incapacity to keep consumers from abandoning its stores for the lower prices and (2) the convenience of online shopping? My own opinion: These two latter reasons are valid, but not the only ones.

The emergence of new substitute’s and the emergence of new e.com-retailers´ substitutes started to provide more benefits to customers not just by lowering prices, but also because the relative price performance from other new alternative retailers was a key determinant factor in the erosion of “Toys R Us” sales. In order to compete with “all substitutes retailers”, “Toys R Us” tried an “omnichannel strategy”. Can you imagine, the huge amount of retailers which were selling toys? It is overwhelming to compete as such with so many retailer industry groups, particularly when the company was not re-investing its cash flows for doing impact in their sales channel operations, but also for paying high burdens of debt service (interest and principal repayments). “Toys R Us” faces a long-term debt totaling more than $5.2 billion.

Source: Forbes.com

Do you think “Toys R Us” missed the opportunity to develop its own e-commerce presence with its Amazon strategic alliance in the 1990s? “Toys R Us” leaders knew Amazon was offering a good alternative since the beginning. Even though the alliance did not work out well. But let´s face it: to keep an omnichannel distribution sales strategy is not easy, we need enough investing in capital expenditures not just to originate new sales distribution channels, but to keep it functioning well… and “Toys R Us” were not experts in logistics and deliveries as Amazon.com or other e-tailers which sell toys as much as they sell clothing, medicines, or electronic devices. There is a learning curve for each sales distribution channel which “Toys R Us” has been learning through the last decades.

Before finishing, let´s return back to analyze the basics, let´s think about what is the core business of “Toys R Us”, and think for a moment about “Toys R Us” value proposition.

All-New Fire 7 Kids Edition Tablet, 7″ Display. Available for $99.99 at Amazon.com

During the last decade, there has been a shift in kids needs and wants. Since electronic tablets and smartphones have been in the market at cheap prices (for less than USD$100 dollars), tablets are easier to buy even for low-income families. Little kids who have access to tablets and smartphones, do not seem interested to play in the park. Little Kids who have a tablet with video games and learning applications, do not seem motivated to play with dogs outside next to trees and nature. Little kids do not seem to be interested to interact with other kids outside the home and do not seem to have fun by playing with other kids, or with mud or even to build Lego cities anymore. Little by little, toys have been substituted by electronic devices. I wonder if “Toys R Us” decided to drop fighting for the continuity of its operations in the USA, just because their old value proposition doesn´t fit with the future of their new kid clients. The kids of today do not believe in the traditional toys from our parents and my generation anymore. Can we start to design new toys for the new kids “wants and needs” which can compete against tablet games, smartphones, and electronic applications? How to rescue the best of Generation X toys for the kids of today and tomorrow?

What do you think?